Tariff Shocks, Hormuz Blockade, and the Cracking of the Trump Coalition

As May Day protests erupted from Paris to global capitals on May 1, 2026, the converging pressures of tariff-driven economic disruption, a blockade tightening global oil supply, and a right-wing media fracture around Donald Trump are reshaping the international order in ways that may prove irreversible.

On the first of May 2026, May Day protests in Paris dissolved into running battles between demonstrators and police. Across the world, on the same day, the Trump administration released figures claiming it had achieved consumer price reductions running to 600, 800 — even higher — percent. The two events occupied different registers, but they shared a common pressure point: the tariff regime that has unsettled global trade architecture since the second Trump administration took office.

The Paris street violence was not simply a French story. It was the visible surface of a larger wave of economic anxiety that has produced protests in Chicago, Berlin, São Paulo, and Seoul over the preceding months. Workers in export-oriented economies, consumers in import-dependent nations, and trading partners facing Washington's tariff schedule have all felt the tremors. What Paris revealed on May 1 was the political temperature rising at the point where economic disruption meets institutional friction.

The administration has consistently framed the tariff escalation as a negotiating tool rather than a permanent restructuring — a pressure campaign whose yield would be lower trade barriers and cheaper consumer goods. Trump's May 1 claim that the United States was delivering reductions of 600 to 800 percent went further than usual, and the figures were met with skepticism from independent economists who noted that no tariff reduction of that magnitude has been formally enacted or documented in any public tariff schedule. The White House has pointed to bilateral agreements and suspended tariff tranches as evidence of progress, but the claimed percentage reductions — multiples of the pre-existing tariff baseline — exceed what the negotiating record supports. The gap between the political framing and the published tariff schedules has become a growing area of media scrutiny, with multiple outlets noting that the administration's price-cut narrative requires assumptions about pass-through and bilateral offset agreements that have not been independently verified.

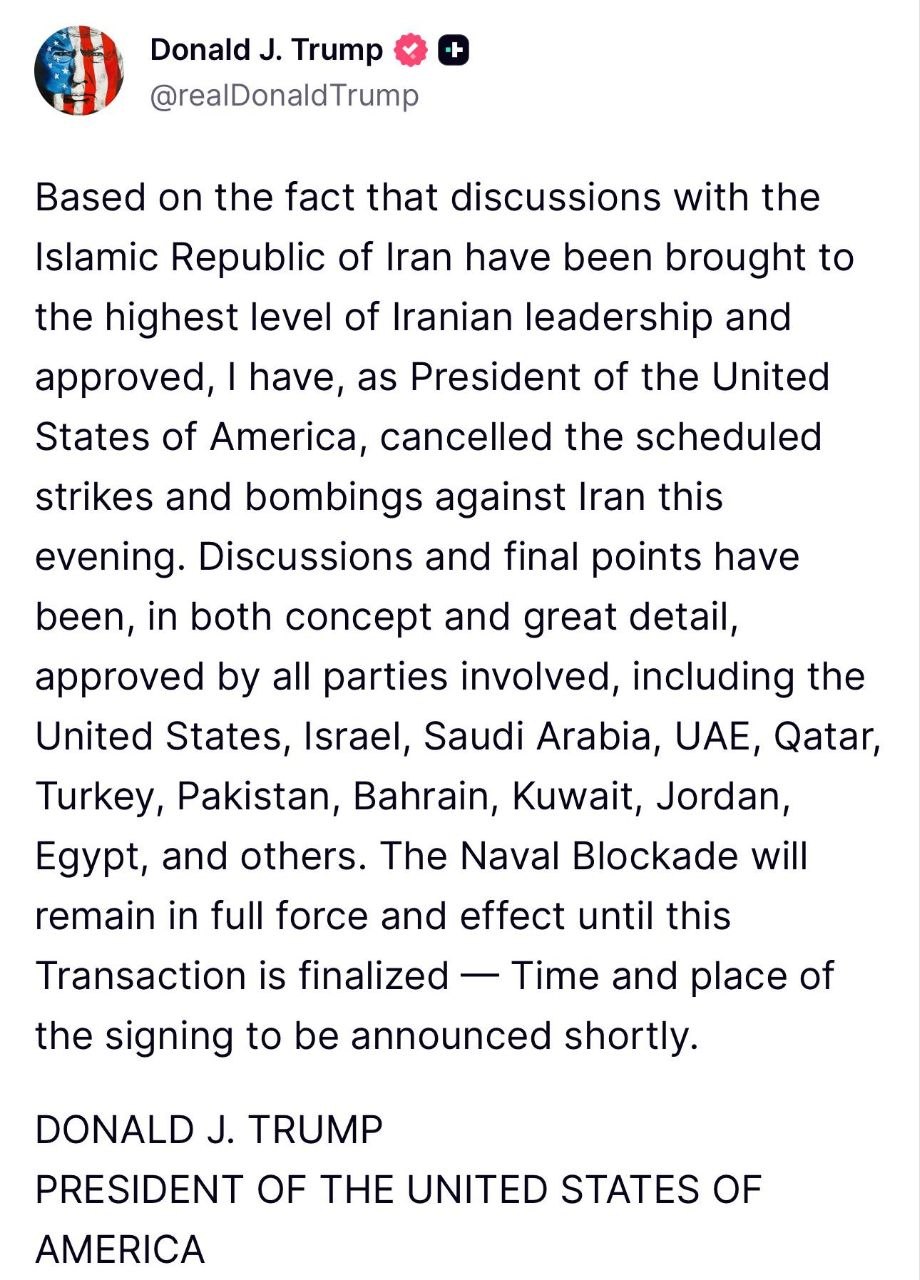

The Hormuz blockade presents a separate and more acute pressure. On May 1, 2026, Polymarket trading data indicated that market participants assigned a high probability to the blockade remaining in place through the month. The strait carries roughly a fifth of the world's liquid natural gas and a substantial share of global oil shipments. A prolonged blockade does not merely raise prices — it introduces structural uncertainty into long-term contracting, hedging, and insurance markets. Shippers have reportedly demanded war-risk surcharges; classification societies have reviewed coverage terms. These are the mechanisms through which supply anxiety translates into price spikes that reach consumer markets within weeks.

Iran has characterised the blockade as an act of economic warfare that, while stopping short of open conflict, constrains the country's legitimate trade and is designed to produce capitulation through strangulation rather than confrontation. That framing has found a degree of sympathy in capitals beyond those conventionally aligned with Tehran — not as support for Iran's policies, but as recognition that unilateral maritime enforcement actions without a United Nations mandate set precedents that smaller states cannot ignore. The absence of a diplomatic off-ramp is itself a risk factor. The administration has indicated it views the blockade as leverage and regards its removal as a concession. Iranian officials have said they view any signal of reduced resistance as weakness that invites further escalation. That binary creates space for miscalculation as long as both sides treat any de-escalatory signal as a trap rather than a beginning.

The political costs of the tariff-and-confrontation posture have begun to surface in the United States itself. On April 26, 2026, Tucker Carlson posted a public apology for his past support of Donald Trump — a break that, given Carlson's sustained role as a principal amplifer of the Trump message during the first term and much of the second, carries structural weight. The apology cited the material consequences of the administration's economic policies — specifically, the cost increases and job disruptions that the tariff programme has produced in communities Carlson had explicitly appealed to as his core audience. For a media figure whose brand has been built on economic populism directed at working-class Americans, acknowledging that the administration's signature economic programme has produced measurable harm to those same communities is not a minor rhetorical adjustment. It is a diagnostic of where the coalition's internal contradictions have reached an inflection point.

Carlson is not alone in that fracture. Several high-profile figures who built their political identities around Trump over the preceding years have issued public reservations, qualifications, or explicit divergences in the weeks preceding May 1. The pattern suggests a coalition held together not by a shared policy position but by a shared opposition and a set of aesthetic commitments that are proving less durable when tested against observable outcomes. When the costs of the programme become visible — in price tags, layoff notices, and shipping delays — the aesthetic becomes harder to maintain. The question is not whether the coalition fractures but in which direction, and whether the administration responds by adjusting its course or tightening its grip on the narrative.

The convergence of these pressures — street protests in Paris, a disputed price-cut claim from Washington, a Hormuz blockade that is reshaping global energy risk premiums, and a prominent media defection from the Trump coalition — is not coincidental. Each is a response to the same underlying shift: the tariff strategy and its companion postures have moved from negotiating theatre to structural reality. The disruption is no longer speculative; it is showing up in shipping data, insurance markets, consumer price indices, and street-level protests.

That reality is beginning to alter calculations beyond the immediate political arena. Trading partners who initially treated the tariff escalation as a bluster-and-negotiate cycle are recalibrating their exposure to a regime whose stated goal may have shifted from renegotiation to restructuring. The Hormuz blockade reinforces the signal: leverage deployed without apparent concern for secondary consequences is changing the calculus of dollar-denominated trade and dollar-infrastructure dependence. These structural shifts do not automatically produce a realigned order, but they produce the conditions in which realignment becomes thinkable for actors who previously considered it impractical.

What remains genuinely uncertain is whether the administration has a coherent exit from the posture it has adopted, or whether the pressures are compounding faster than any internal recalculation can be made operational. The Polymarket data reflects market sentiment at a specific moment; it is not a prediction of policy. But it is a signal that the actors who manage financial exposure are pricing in continuity, not resolution. That pricing discipline — cold, probabilistic, and indifferent to political messaging — may prove to be the most accurate description of where the situation is actually headed.

This publication covered the convergence of May 1 protests, the Hormuz blockade, and the tariff-fray narrative as related signals of a global order under structural stress rather than as isolated events. The Hormuz Polymarket market was cited to capture the financial-market pricing of continued blockade, a signal not typically foregrounded in wire coverage of the strait's politics.