The Strait at the Center of Everything

Iran's new Hormuz management mechanism and persistent attacks on vessels suggest the global economy's most critical chokepoint is becoming a permanent risk premium — not a temporary shock.

Something has broken in the global supply chain that money alone cannot fix. On 5 May 2026, Iran unveiled a new mechanism for managing vessel transit through the Strait of Hormuz — the 21-mile-wide waterway through which roughly 20 percent of global oil shipments pass. One day later, the UAE reported additional attacks from Iran, even as Washington declared the ceasefire holding. The Polymarket odds on Hormuz traffic normalizing by month's end sat at 22 percent. These data points, taken together, suggest a world that has not fully reckoned with what a permanently disrupted Hormuz actually means.

The IMF's assessment, published by CGTN on 5 May 2026, is unambiguous: the conflict is producing a "much worse outcome" for the global economy than baseline forecasts had modeled. Brazil's central bank went further on 6 May 2026, warning that emerging market inflation risks are building as the war drags on — a transmission mechanism that will disproportionately hit the Global South, where dollar-denominated debt burdens amplify every commodity price spike. This is the structural story that commodity price charts and ceasefire headlines have obscured: the Hormuz chokepoint is not returning to baseline, and the global economy has not priced accordingly.

A Chokepoint Under Permanent Pressure

The Strait of Hormuz is not merely a shipping lane. It is the world's most concentrated single point of energy transit. Any disruption to throughput — whether from military activity, Iranian inspection regimes, or insurance market recalibration — translates into elevated freight costs and elevated energy prices. The conflict has given Iran a rationale and a tool to manage that throughput on its own terms. The new management mechanism is not a blockade in the classical sense; it is something more ambiguous, and therefore more durable. Vessels face delays, inspections, and political conditionality rather than outright denial of passage. The result is a friction premium, not a hard stop.

That friction premium compounds. Brazil's central bank identified the mechanism on 6 May 2026: commodity price shocks transmit through supply chains with a lag, and emerging economies with dollar-denominated import bills feel the second and third-order effects most acutely. The IMF warning from CGTN on 5 May 2026 frames this as a global phenomenon, but the distributional arithmetic is not neutral. US consumers, as one financial analysis noted, are bearing the frontline burden of the inflationary transmission — not because American wages are uniquely exposed, but because dollar hegemony means commodity price shocks denominated in dollars land first and hardest in the US economy.

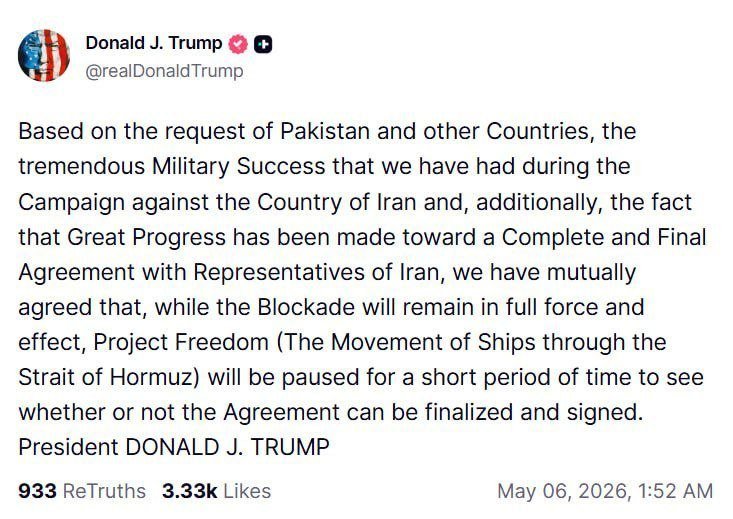

The Ceasefire That Isn't Holding

Washington's characterization of the ceasefire as holding sits in evident tension with the evidence. On 6 May 2026, the UAE reported additional Iranian attacks — a direct contradiction of the stability framing. Iranian state-adjacent commentary noted that events in the Hormuz corridor demonstrate a military solution to a political crisis is not viable, a framing that implicitly acknowledges the blockade's political logic rather than any desire to resolve the underlying dispute.

The Polymarket odds reflect rational market uncertainty rather than confidence. A 22 percent probability of normalization by end of May implies a 78 percent probability that friction continues — that Iranian conditions on transit persist, that inspections and delays remain the operational reality, and that shippers must price in a permanent risk premium. Insurance markets, freight derivatives, and energy forward curves are already moving to price that premium. The ceasefire headline has not changed the structural fact: Iran controls one of the world's most critical chokepoints, and the conflict's political logic has not been resolved.

The Multipolar Arithmetic

What the Western wire framing has struggled to capture is the geopolitical distribution of costs. The conflict is accelerating a fragmentation already underway in global trade architecture. Shippers routing around the Cape of Good Hope face longer transit times and higher fuel costs — a tax on the global commons that disproportionately benefits alternative routes, alternative energy suppliers, and alternative financial architectures. Russia, already positioned as a fallback energy supplier for countries willing to accept dollar-discounted crude, gains further leverage. Gulf states whose fiscal budgets depend on barrel prices have a structural interest in sustained disruption short of total collapse.

The irony is that the global economy's dependence on a single, contested corridor for 20 percent of its oil shipments was always a fragility — not a design choice. The conflict has simply made that fragility legible. The question is not whether the system is resilient but whether the political will exists to diversify the energy transit architecture before the next Hormuz crisis arrives.

Who Bears the Cost, and for How Long

The stakes are concrete. A sustained friction premium at Hormuz means elevated energy prices baked into global supply chains for months, not weeks. It means inflation pressure that constrains monetary policy in economies already stretched by debt service. It means Brazil, South Africa, Egypt, and other import-dependent emerging markets absorbing shocks the IMF's models have consistently underestimated.

The United States, as one analysis put it, is bearing the frontline burden — not as charity, but as the structural consequence of a dollar-denominated global economy that has no credible substitute for Gulf energy transit. The ceasefire is shaky because the political architecture that would produce a durable resolution does not exist. Until either a negotiated transit framework or a credible deterrence posture changes that equation, the Hormuz premium stays priced in.

The world has absorbed a great deal from this conflict. What it has not done is adapt. That adaptation — rerouted supply chains, diversified energy transit, restructured dollar exposure — is the next phase of a disruption that the ceasefire, as currently understood, has done nothing to resolve.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- http://reut.rs/4we3sKJ

- http://reut.rs/4n9J4q9

- http://reut.rs/42hUyOz