The $7 Billion Bet on Middle East Fire

Something worth noting surfaced in the financial data on 7 May: well-timed positions in crude, gasoline, and diesel futures ahead of major Iran-war announcements totaled at least $7 billion, according to Reuters reporting. That figure — described as far exceeding earlier estimates — has received a fraction of the attention devoted to the military exchanges it presaged.

The gap in coverage is instructive. When a missile barrage in the Strait of Hormuz drives a spike in Brent crude, the market move is treated as a consequence. The positions taken before the announcement are treated as coincidence. They deserve more scrutiny.

A Convenient Timing

The Reuters figures are specific and the timing is narrow: positions placed in energy futures in the days immediately preceding announcements from Washington or Tehran that moved markets. The $7 billion aggregate encompasses crude, gasoline, and diesel contracts across exchanges. Sources describe the volume as unusual even by the standards of a market that has priced Middle East risk for two decades.

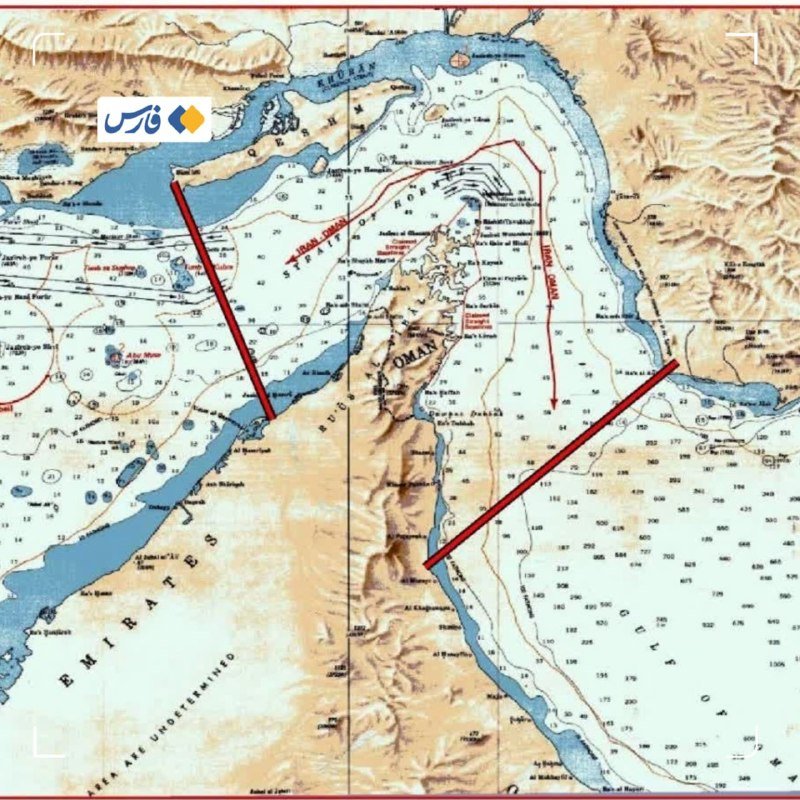

The BBC reported on 8 May that oil prices rose after US and Iranian forces exchanged fire in the Strait of Hormuz — the same waterway through which roughly a fifth of the world's oil passes. The flare-up further endangered the US-Iran ceasefire that President Trump extended indefinitely on 21 April. Separate reporting from Iranian military sources, cited by open-source monitors on 7 May, claimed Iran fired missiles at US forces after US troops attacked an Iranian oil tanker in the strait.

If the sequence holds — positions placed, announcement made, prices moved — the trade is legible. What remains unclear is the mechanism. Were these positions placed by entities with access to intelligence about pending announcements? By regional actors with better sightlines to escalation timelines than Western markets assumed? By algorithms that detected pre-announcement patterns invisible to human traders? The sources do not specify. That ambiguity does not make the question go away.

China's Calculated Hedge

The same Reuters poll that flagged the derivatives positioning also documented China's export data for April 2026. The figures likely show export growth accelerated that month, partly driven by demand for goods — fuel, machinery, dual-use materiel — associated with war-economy stockpiling. The Iran conflict, now in its acute phase, has disrupted supply chains and prompted regional states to accelerate imports of everything from refined petroleum products to industrial inputs.

Beijing has not publicly aligned itself with either Washington or Tehran. It has also not concealed its interest in stable energy flows or its willingness to supply both sides of a conflict through commercial channels. The export data is consistent with a China that is profiting from the disruption without being consumed by it — a structural position the Chinese development model is well-equipped to exploit. Where Western analysis tends to frame this as opportunism, the Chinese framing frames it as commercial pragmatism conducted within international trade law. Both framings have merit.

The Hormuz Premium

The Strait of Hormuz sits at the intersection of several structural pressures that predate the current escalation. It is the world's most critical oil transit chokepoint; it sits between two US-aligned Gulf monarchies and an Iranian state that has spent four decades building counterbalance capacity, including anti-ship missiles and drone swarms. Any serious analyst of Gulf security has flagged Hormuz vulnerability as a first-order risk for global energy markets.

What changed in April 2026 was not the underlying risk architecture but the frequency and lethality of the incidents. The ceasefire Trump announced in January, then extended on 21 April, was always a fragile arrangement. The 7 May exchange — US forces striking an Iranian tanker, Iranian missiles fired in response — is the kind of incident that breaks ceasefires. The Reuters data on derivative positions suggests that some market participants were positioned for exactly that outcome before it was publicly confirmed.

What the Numbers Cannot Tell Us

The $7 billion figure is a floor, not a ceiling. The Reuters reporting covers futures contracts on major exchanges; it does not capture bilateral over-the-counter positions, options structures, or physical tanker contracts that might carry directional exposure to Hormuz disruption. The identity of the counterparties is not specified in the available reporting, and it would be irresponsible to speculate.

What can be said is this: when the gap between anticipated and realized outcomes in a geopolitical event is systematically profitable, the market is functioning as an information-arbitrage mechanism — or as an indicator that some participants had better information than others. Both readings are unflattering to the assumption that markets price Middle East risk on an even information field.

The $7 billion also does not account for the human dimension. Each exchange in the strait raises the probability of an incident that closes the waterway entirely — not a remote possibility but a contingency Gulf states and their trading partners have war-gamed for years. The financial positions are a derivative of that risk. The risk itself is not a derivative of anything.

This publication has documented how financial markets absorb geopolitical shock; the derivative data is a useful lens. But it is worth holding the lens up to the light and asking who made the bet, who funded the intelligence that timed it, and who will pay the premium if the strait closes. The $7 billion is not the end of that inquiry — it is the opening question.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- http://reut.rs/4ngGY7L