Iran's Stock Market Opened Today. The Ceasefire's First Verdict Is In.

Tehran's exchange closed in positive territory on its first trading day since the conflict began — a signal that markets expect the peace talks to hold. The numbers tell a more complicated story.

On 19 May 2026, Iran's Tehran Stock Exchange opened for the first time since the conflict with Israel began — and closed the day in positive territory. That is the first market verdict on the ceasefire. It will not be the last.

The rally tells us something real: traders in Tehran believe the talks will hold long enough to justify re-entry. But it also tells us something about the structural pressures the ceasefire was designed to relieve — and the far larger pressures it has not resolved. The peace on the table is a pause, not a settlement. Iran's negotiating position, its reparations demands, its insistence on American troop withdrawal, makes that distinction clear.

Markets Pronounce First

When a stock exchange opens after weeks of silence, the closing number is a statement. A green session on the first day back is not neutral. It signals that participants believe liquidity can return, that trade corridors can reopen, that the worst of the economic contraction is behind them. Iranian markets had been shuttered under wartime operating protocols — a move that itself revealed how deeply the conflict had disrupted even the most basic financial infrastructure of a country of 88 million people.

The Reuters reporting on Iran's peace proposal makes the stakes of that reopening explicit. According to reporting filed on 19 May 2026, Tehran's negotiating framework includes a demand for reparations covering war damages — and a parallel demand for the withdrawal of American forces from the region. These are not baseline ceasefire conditions. They are victory terms. The question is whether the ceasefire represents the first step toward that outcome, or the ceiling.

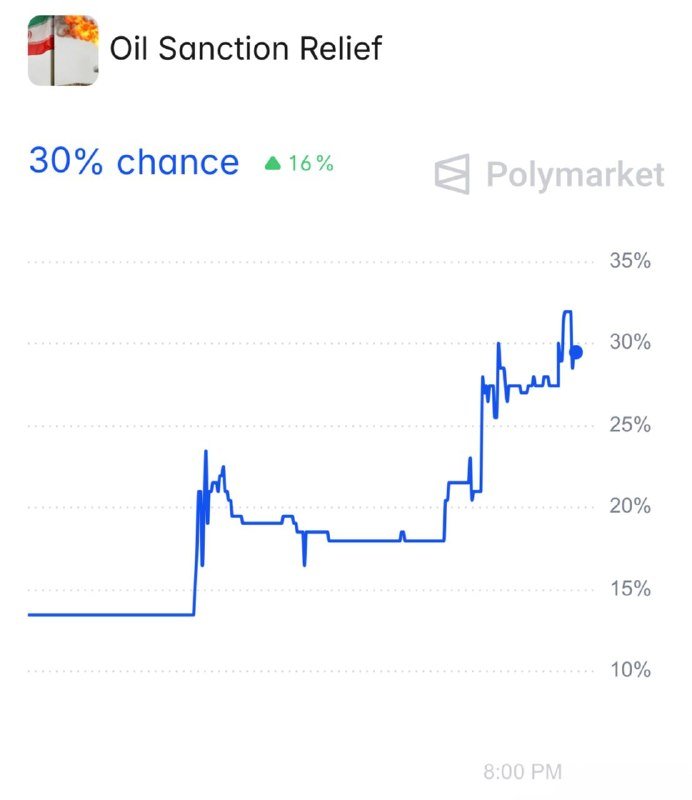

The Polymarket data circulating this week — a 39 percent implied probability of Iran closing its own airspace by the end of next month — is the market's honest admission of uncertainty. Forty-one percent odds of airspace closure, after a ceasefire, suggests traders are not treating this as a settled trajectory. They are pricing in the possibility that the same dynamics that produced the conflict have not been resolved, merely paused.

The Ceasefire's Structural Logic

What produced this pause is not goodwill — it is exhaustion, on both sides. Iran's economy has absorbed sanctions pressure, energy sector disruption, and the closure of its own stock exchange. Israel's economic exposure, through Gulf maritime disruption and regional escalation costs, has also been significant. A ceasefire is the rational move when continuing is more expensive than stopping. That is not the same as peace.

The reparations demand is the structural tell. When a party demands compensation for war damages, they are not negotiating a technical end-of-hostilities. They are positioning for the legal architecture of the aftermath — compensation frameworks, sanctions relief sequencing, asset解凍. Iran is building the case for a settlement that treats it as the aggrieved party with legitimate claims, not a pariah state that lost a conflict.

That framing has strategic value well beyond the financial. It reframes the regional dynamic from one of Iranian isolation to one of contested sovereignty. It shifts the legal and diplomatic ground on which future negotiations will be conducted. And it puts Western capitals in the position of either engaging with that framing or explaining why Iranian reparations claims — after a conflict that caused demonstrable civilian and infrastructure harm — are categorically different from the claims that Western governments have upheld in other post-war contexts.

The American troop withdrawal demand is more blunt. It is an attempt to alter the regional balance of power through the peace process itself. If American forces leave, the deterrence architecture that has constrained Iranian regional behaviour for decades changes shape. That is the prize Tehran is angling for — and it explains why the ceasefire is less a resolution than a renegotiation of the regional order.

Energy Markets Already Moving

The BBC reported on 19 May 2026 that unleaded petrol prices in the UK had reached their highest level since the conflict began. The RAC, the British roadside assistance organisation, warned of further increases in the coming weeks. This is the ceasefire's first downstream economic signal — and it will not be confined to Britain.

Oil markets have been pricing conflict risk for weeks. A formal ceasefire removes the acute supply disruption premium but does not restore the pre-conflict baseline. Iranian production capacity has been impaired. Iranian-aligned maritime risk in the Strait of Hormuz has not disappeared. And the broader sanctions architecture that constrains Iran's oil exports remains intact unless the peace talks produce a formal sanctions relief agreement.

The structural picture is one of constrained supply and elevated floor prices. The ceasefire reduces the upside risk — it removes the acute escalation premium — but it does not restore the supply capacity that was damaged during the conflict. Energy consumers in Europe, in Asia, and in the Global South are absorbing the cost of a conflict they did not start and a peace that has not yet delivered relief at the pump.

The Airspace Question

The 39 percent Polymarket probability on airspace closure by end of next month is the most honest metric in this picture. It suggests that a substantial minority of market participants — or geopolitical watchers — do not believe the ceasefire resolves the underlying instability. That is a reasonable read.

Airspace closure requires a state decision. It is not a by-product of conflict; it is a deliberate act of sovereignty assertion. If Iran closes its airspace — to military overflights, to commercial traffic, or to some combination — it will be making a political statement that the ceasefire does not bind Iranian strategic choices going forward. That would put the peace process in immediate jeopardy.

The alternative reading — that the ceasefire will hold, that Iran will negotiate in good faith, that the reparations and withdrawal demands are opening positions rather than red lines — requires believing that both parties have shifted from the strategic logic that produced the conflict. The stock market rally suggests Tehran believes that. The Polymarket pricing suggests the market is less certain.

Both readings may be correct, at different timescales. A ceasefire that holds for six months is not the same as a settlement that holds for thirty years. The stock market's green close on 19 May 2026 is a bet on the short run. The longer run is still being written — and it will not be written on the trading floor.

This piece was drafted from wire sources only; no academic or theoretical frameworks were applied to the structural framing.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/Middle_East_Spectator/placeholder

- http://reut.rs/43nho7P

- https://t.me/IRIran_Military/placeholder