The Iran War's Fiscal Dividend: How Moscow Turns Conflict Into Cash

As the Trump administration escalates pressure on Tehran, Russia is quietly collecting the proceeds. A 39 percent surge in oil and gas revenue is the unexpected consequence of a conflict that Washington insists is popular at home.

There is a peculiar arithmetic to great-power competition that the Trump administration has yet to reckon with: when you destabilize a region, you do not always destabilize your adversaries. According to data reviewed by Reuters on 20 May 2026, Russia's oil and gas revenue is projected to rise 39 percent year-on-year in May. The proximate cause, the reporting suggests, is the disruption cascading from the Iran conflict. Moscow is collecting what amounts to a fiscal subsidy from a war it did not start — and one that Washington insists serves American interests.

The numbers are not ambiguous. A near-two-fifths increase in hydrocarbon revenue gives the Kremlin fiscal room it has not had since the pre-2022 sanctions architecture tightened. Whether that revenue bump reflects higher global prices driven by supply uncertainty, increased volumes sold at a discount through third-country intermediaries, or a combination of both, the outcome is the same: Russia is financially better positioned because the Middle East is on fire. The administration has framed its Iran policy as strength. The balance sheet tells a different story.

Iran Sees a Coordinated Campaign

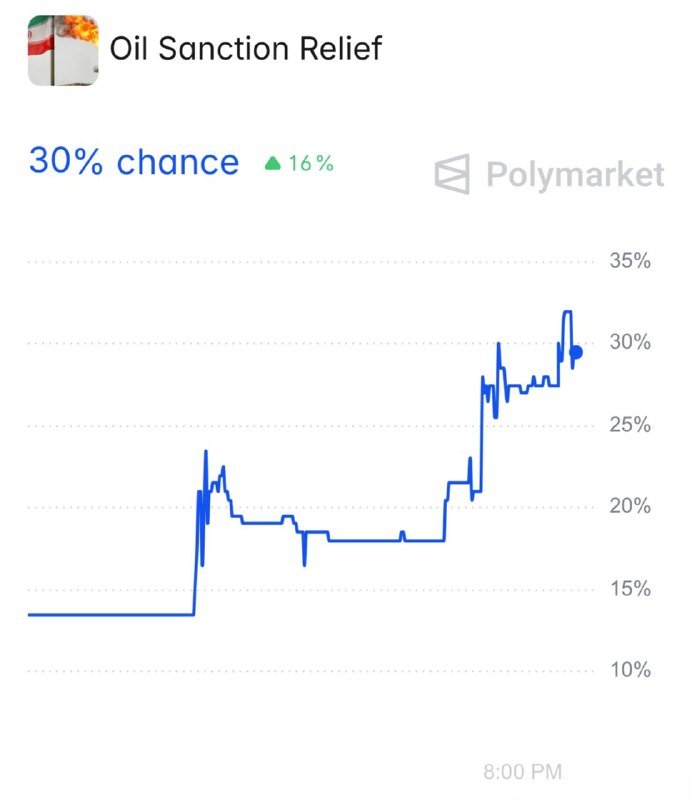

Tehran's framing of recent events matters. Iranian state media, cited by monitoring outlets on 20 May 2026, described the enemy as "seeking a new round of war." That language is deliberately maximalist — the Islamic Republic deploys existential framing as a matter of course — but the underlying perception has structural logic. From Tehran's vantage, the sequence of maximum-pressure re-escalation, the killing of Qasem Soleimani's successors, and the targeting of nuclear infrastructure constitutes a coherent campaign rather than a series of disconnected moves. Iran is not wrong to read coordinated intent.

The difficulty for Western analysts is that this perception, however filtered through regime propaganda, describes a material reality. The Islamic Republic faces economic strangulation, military probing, and diplomatic isolation simultaneously. That combination is designed to break the regime's will — but it also removes any internal constituency for the kind of managed, transactional diplomacy that might have preserved a narrow lane for de-escalation. Tehran now has little incentive to bargain and every incentive to fight the conflict out. The administration's insistence that Iran is "begging to make a deal," attributed to Trump on 19 May 2026, sits in direct tension with Iranian official statements rejecting further concessions.

The Popularity Calculus

Trump's own assessment of the Iran campaign, also reported on 19 May 2026, acknowledged that advisors warned him the conflict was politically unpopular — then expressed confidence it was nonetheless "very popular." That self-confidence is not a policy argument. It is a claim about domestic approval that cannot be verified independently and that contradicts the pattern of polling data on Middle East military engagement that has accumulated over twenty years of American public opinion research. The gap between the administration's conviction and measurable public sentiment is itself a data point: the executive branch is proceeding on its own calculus, unmoored from the electoral accountability it claims to cherish.

This matters because the costs of the Iran escalation are not abstract. Higher energy prices — the mechanism by which Russia benefits — flow directly to American households and businesses in the form of elevated fuel costs and imported goods inflation. The administration is asking Americans to absorb real economic pain for a geopolitical outcome that is at best contested and at worst counterproductive. The political logic assumes a payoff visible enough to change minds. There is no evidence yet that such a payoff is coming.

The Structural Consequence: Funding the Adversary

The deeper problem with the current trajectory is one of incentive architecture. The United States has, across multiple administrations, pursued a version of pressure-maximization against Iran that operates on the assumption that economic pain produces political capitulation. That assumption has now been stress-tested across two decades of sanctions with no regime change to show for it. What it has produced is a regional alignment of convenience between Tehran, Moscow, and Beijing structured around shared opposition to American hegemony. Every escalation narrows the diplomatic lane and deepens that alignment.

Russia's 39 percent revenue surge is the most recent example of a pattern that should concern any serious student of American foreign policy. The tools the United States uses to punish adversaries produce, with notable regularity, unintended financial transfers to precisely the actors it seeks to weaken. The mechanism is not mysterious: disrupting Middle Eastern oil flows raises global benchmarks, and Russia — which cannot be expelled from the global energy market given its structural position in Asian demand — sells into a higher-priced market as a result. The sanctions regime designed to strangle Russian state revenue is being undermined by an unrelated conflict policy.

The beneficiaries of this particular dynamic are specific and named: the Kremlin gets fiscal space to sustain its military operations in Ukraine; Russian state enterprises get harder currency at improved terms; the political logic that says "maximum pressure" works receives empirical confirmation that it does the opposite. None of this is hypothetical. It is arithmetic.

What Has Not Worked

The administration has not articulated a theory of victory in Iran that survives contact with the facts on the ground. Regime change — the implied goal of sustained maximum pressure — has not occurred despite the most intense sanctions campaign in modern history. Negotiated freeze — the alternative — requires a willing partner, and Iran has concluded it has no reason to be that partner. Drone and missile strikes have degraded infrastructure but not will. The result is a conflict that is neither won nor ended, whose costs are borne disproportionately by the American consumer and the Russian state treasury respectively.

What remains uncertain is whether the administration has a viable off-ramp that does not require Tehran to credibly threaten resumed nuclear work as a bargaining chip — which is precisely the dynamic that maximum pressure was meant to prevent. The sources reviewed for this piece do not specify what diplomatic back-channels exist, whether any are active, or what a face-saving de-escalation framework might look like. The absence of that information is not a rhetorical gap. It is a material one. Until there is evidence of a negotiated end-state, the policy remains a mechanism for transferring wealth to adversaries while claiming strength.

The irony is not subtle: a war meant to weaken Iran is funding Russia. That outcome deserves to be described plainly, not softened into diplomatic abstraction.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- http://reut.rs/4fsq5oM

- https://twitter.com/unusual_whales/status/1921574467848511488

- https://twitter.com/unusual_whales/status/1921468524268720641

- https://twitter.com/unusual_whales/status/1921458137869271553